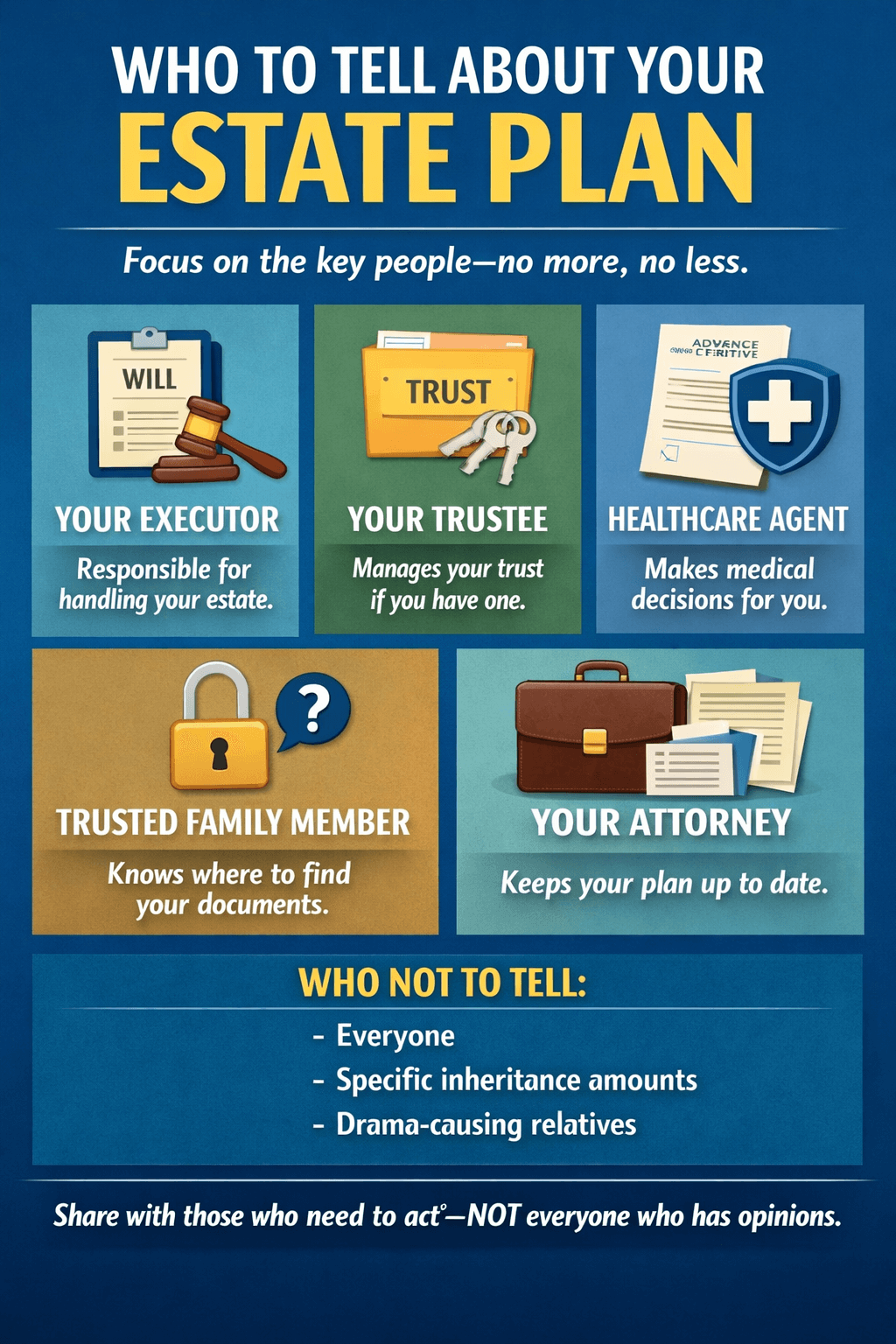

People often have a ready list of reasons—or depending on how you look at it, excuses—for putting off completing their estate plan: “I just haven’t gotten around to it yet”; “I don’t own anything of value”; “It’s too complicated”; “It’s too expensive”; “My family can handle things when I’m gone”; or “I’ll wait until I’m older and really need one.” These attitudes are reflected in the numbers; most Americans have no estate plan, and many do not intend to create one.1

However, lurking beneath the surface is perhaps a more powerful and all-encompassing motivation for their inaction: a desire to avoid the complex emotions that often accompany estate planning.

Estate planning requires confronting emotionally charged topics. While thinking about your potential incapacity (inability to manage your own affairs) or death may be unsettling, avoiding uncomfortable topics and the feelings they trigger can often make the situation worse for you and your loved ones.

Instead of avoiding these topics, try to recognize and reframe the estate planning process as the opportunity to take control and create something positive and productive. You will feel more empowered by taking action now, and your family will thank you later.

Why We Avoid Estate Planning: The Psychology Behind “Not Yet”

Estate planning is not merely a legal process; it is also an emotional one.

Some people may admit that they would “rather not think about” estate planning or they are “not ready yet.” But among those who keep putting off their plan, chances are that estate planning is never far from their mind, at least indirectly.

A 2025 survey found that nearly one in five people think about their own death at least once daily and about two-thirds have given serious thought to their end-of-life arrangements.2 Many have even decided on the details of how they want to be buried (29 percent), the location of their final resting place (19 percent), and the type of service they want (17 percent).3 Fourteen percent said they have even curated their funeral playlist.4

At the same time, death and estate planning ranked as the second-most difficult subject to talk about with loved ones, along with topics such as mental health, past mistakes, and regrets.5 Twenty-five percent of respondents called death and estate planning “uncomfortable.”6

The survey reveals a key barrier to the estate planning process: thinking about death privately and discussing it with others are two very different things.

While avoiding topics that spark complex emotions may feel easier in the short term, it can reinforce negative feelings over time and make it harder to act on important matters, including estate planning, even when you know it is necessary.

However, the same emotions that make estate planning difficult can become the very means that help you complete it—if you learn how to appropriately reframe your feelings.

Turning a Negative into a Positive: Estate Planning and Emotional Reframes

Emotion and cognition are closely linked. Strong emotions make it harder to think and act by disrupting the very processes required to analyze problems and identify possible solutions.

Psychological research indicates that naming and reframing emotions can enhance emotional regulation, sharpen thinking, and improve decision quality.

This approach, known as cognitive reappraisal, involves changing how you interpret a situation to alter its emotional impact.7 By focusing on aspects of a situation that evoke positive emotions rather than negative ones, you make it easier to solve problems and achieve your goals.

In the context of estate planning, you should not be expected to ignore difficult emotions. In fact, these strong emotions often mean that what you are doing truly matters. Denying your emotions can hinder progress, while reframing them as useful signals can help you move forward.

In practice, applying cognitive reappraisal to estate planning might look something like this:

- Fear → Control and Readiness

Fear often arises when the unknown feels bigger than what we can manage. Reframing it as a cue to gain control by organizing documents, clarifying intentions, and identifying decision-makers can help transform fear into action. Fear, in this light, becomes the starting point for readiness. - Sadness → Legacy and Meaning

Sadness often appears because of real or perceived loss, but it can also reveal what matters most to you. By channeling that emotion into expressing your legacy—writing letters, creating trusts for loved ones, or supporting causes that reflect your values—you can turn grief into purpose. - Anger → Fairness and Clarity

Anger often grows from family conflicts, blended family tensions, or perceived injustices. Reframing anger as a drive toward fairness and clarity enables that energy to fuel precise, balanced planning, which reduces later confusion and conflict. - Anxiety → Preparedness and Confidence

Anxiety often stems from uncertainty. By naming what worries you, such as finances, taxes, and medical decisions, and directly addressing those issues in your plan, you replace vague dread with concrete action and certainty. Each completed step reinforces calm and confidence.

Ultimately, the goal of cognitive reappraisal is to turn negative emotions such as anger, fear, and sadness into positive ones, including happiness, peace, and joy: happiness that you finally got your plan together, the peace of mind that comes from transforming uncertainty into vision, and the joy of knowing that your loved ones will be taken care of and protected when you are gone.

The process itself can be a powerful act of self-understanding. If, at the end of it, you feel lighter, calmer, or more at peace, it is because of the relief that comes from clarity and resolution, not from avoidance, denial, or wishful thinking. You have faced something difficult and deeply human, taking control not just of your money and property, but also of your narrative and legacy.

Be Courageous and Meet with Us

There is an idea in philosophy that all stories are ultimately about fear of death and reflect our struggle to face mortality. A similar psychological truth might explain why so many people hesitate to create an estate plan.

Even when they do, the process often touches every emotional nerve. It can surface old family conflict, unspoken expectations, and differing ideas of what is “fair.” It asks us to imagine a world without ourselves in it, to assign value to what we have built, and to make choices that may please some loved ones but not others. That is a tall emotional order, even for the most pragmatic person.

But estate planning can also bring moments of connection, reflection, and gratitude. It can stir up difficult emotions—and resolve them as well. The difference ultimately lies in your perception.

Estate planning is more than paperwork. It is an act of courage. A simple reframe may be all you need to take that next step and meet with an attorney to help you address your feelings and channel emotions into action. If you are ready to name and reframe those emotions and take charge of your legacy, call us.

- Victoria Lurie, 2025 Wills and Estate Planning Study, Caring (Sept. 17, 2025), https://www.caring.com/resources/wills-survey. ↩︎

- Two-Thirds Of Americans Have ‘Planned’ Their Funerals, But Majority Avoid Estate Planning Conversations, StudyFinds (Sept. 30, 2025), https://studyfinds.org/americans-planned-funerals-avoid-estate-conversations. ↩︎

- Id. ↩︎

- Id. ↩︎

- Id. ↩︎

- Id. ↩︎

- Cognitive Reappraisal, PsychologyToday, https://www.psychologytoday.com/us/basics/cognitive-reappraisal (last visited Nov. 20, 2025). ↩︎