If your client has already done estate planning by creating a will or trust, then the client has taken a very important step toward ensuring that if the client becomes incapacitated or dies, the client’s loved ones will know how to help manage the client’s financial and legal affairs. However, simply having a will or a trust and related estate planning documents is often not enough. An inventory of all of the client’s accounts and property is crucial for helping the client’s loved ones manage the client’s affairs effectively.

Most estate planning attorneys have received calls from distressed children who know that a deceased parent had a will or a trust, but have no idea what accounts, insurance policies, or items of real and personal property the parent owned. If an inventory was never prepared and shared with the parent’s attorney, the child likely had to spend countless hours meticulously combing through the parent’s file cabinets, drawers, tax returns, and online accounts to identify what the parent owned.

Needless to say, this is not something that anyone wants to happen. Even if a client has not started or completed estate planning, there is no need to wait to prepare an inventory of the client’s property until these legal documents are created. In fact, assembling an inventory can be an excellent first step that encourages a client to begin the estate planning process. This preliminary effort will allow the client to walk into an estate planning attorney’s office and almost immediately begin to focus on creating a will or a trust that takes into account each of the client’s items of property and how they should be coordinated with the client’s estate planning goals. With a complete and accurate inventory in hand, there is little doubt that your client’s attorney will be impressed and grateful for the effort.

Even if your client never gets around to creating a will or trust (of course, this is strongly recommended), a complete inventory of the client’s property will at least help the client’s loved ones quickly identify the property the client owns and the next steps they will need to take in order to gain control of the property and distribute it according to state law. This step alone will significantly reduce the time and costs of administering a client’s estate in the probate courts. And anytime that you, as the advisor, can help a family bring order to chaos, you will increase their trust in you and lay the foundation for future business opportunities with the client’s loved ones and those they may refer to you.

How to Create an Inventory

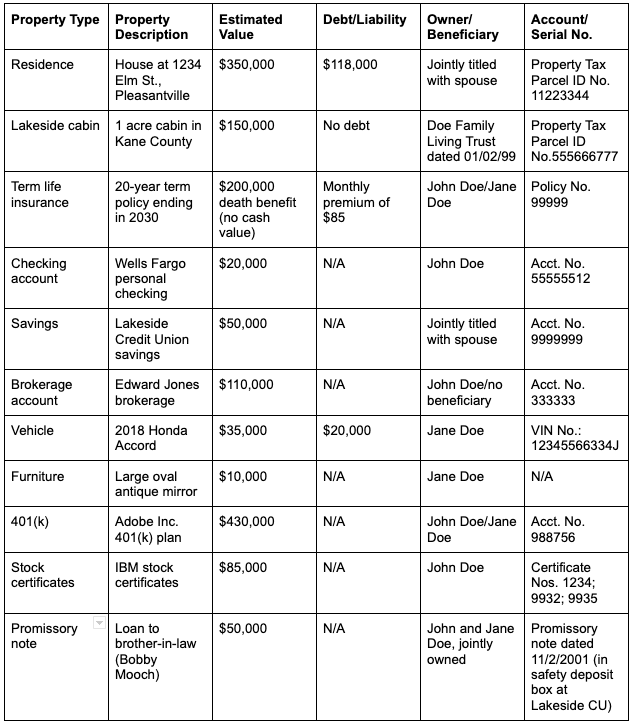

Creating an inventory of a client’s accounts and property need not be terribly complicated. It can be a simple word processing document or even a handwritten list. Many individuals create spreadsheets in software programs like Microsoft Excel, Numbers, or Google Sheets. There are also numerous online services that can help your client create a thorough inventory of the client’s property, store passwords for online accounts, and even store digital copies of a client’s important legal and healthcare documents. Many of these services have features that enable the client to automatically share this information with chosen individuals at a designated time. The bottom line is that any of these above methods can work well—the important thing is that the client prepares an inventory, preferably with your help. Below is an example of an inventory formatted as a spreadsheet with columns and rows:

Of course, this is just an example of what an inventory could look like. The client should include any information that may be helpful to someone who is put in charge of collecting the client’s property after death or disability. The client might also include more details beyond what is shown above, such as where the property is located or even the property’s acquisition value to establish tax basis on the property. For example, if the client keeps certain items of jewelry in a safe, or the client’s boat is stored in dry storage, this would be crucial information to include.

Probate and Your Property

As your client creates the inventory and discovers how each item is titled or who is named as the beneficiary on certain accounts, the client will be able to identify those items of property that will have to go through probate. Probate is the court process that appoints an executor or personal representative to inventory a deceased person’s probate property and distribute it according to state law or the terms of the deceased’s will, if there is one. Generally speaking, any account or property that meets the following conditions will have to go through the probate process: (a) is owned only in the client’s name, (b) is not owned jointly with another person, (c) is not titled in the name of a trust or business entity (like an LLC or partnership), and (d) does not have a named pay-on-death (POD) or transfer-on-death (TOD) beneficiary associated with the property.

As I am sure you are aware, if your client designates beneficiaries on accounts, those beneficiary designations need to be carefully coordinated with the client’s overall plan. For example, the client’s estate planning documents may create trusts for children to provide asset and divorce protection. But, if the client names a child directly, those assets will never flow into that trust, no asset or divorce protection will be achieved, and the client’s goals will not have been met.

Probate can add to the expenses when someone dies, can be time consuming, and is a public process that many people would rather avoid. This is why preparing an inventory well before a client’s death can alert the client to those items of property that will require a probate so that the client can take steps, while still able, to transfer ownership or retitle them in a way that helps the family avoid probate. This might include making sure a beneficiary has been named or establishing a trust into which certain property can be transferred. Again, care needs to be taken to coordinate this with the client’s overall goals and the client should not just blindly list beneficiaries merely to avoid probate.

Additional Benefits of a Complete Inventory

A detailed inventory can help a client’s loved ones understand the next steps to take control of the client’s property for management and distribution. Certain items and accounts, such as the following, may be distributed according to the unique legal aspects of that type of property:

- Property owned in joint tenancy with rights of survivorship (such as real estate or bank accounts) will pass automatically to the surviving joint owner.

- Some bank accounts may have POD or TOD designations that allow for those accounts to skip the probate process.

- Life insurance proceeds typically will not have to go through probate if the client has properly completed the beneficiary designation form by naming loved ones, a trust, or a charitable organization as beneficiaries on the policy.

- Accounts and property titled in the name of a trust can be distributed outside of probate according to the terms of the trust.

- Retirement accounts usually require the listed beneficiaries to file a claim with the account custodian before benefits will be paid out. Probate courts and trusts usually have no control over retirement accounts.

- Vehicles will typically need to be transferred through the local department of motor vehicles, which requires an affidavit along with a death certificate and the physical car title.

- Items of personal property (e.g., furniture, jewelry, art, collections, etc.), if above a certain value as determined by state law, must usually pass through probate, unless they are transferred into a trust before death.

What to Do with the Inventory Once Created

After creating an inventory, do not let the client forget to store a copy where the client’s loved ones will be able to easily access it should something happen to the client. Suggest the following locations as options:

- an estate planning portfolio or binder that is easily accessible to family or friends

- a file folder that is clearly marked and easily accessible

- the client’s file with the client’s estate planning attorney

- an electronic document format that can be shared online with trusted loved ones

- a clearly labeled USB drive in a safety deposit box or safe (as long as the client lets loved ones know what to look for and where to find it)

- the client’s file with you and other professional advisors in the event you are the first one the family calls after your client’s death

Once your client has created and shared the inventory, the client should create a plan for updating. Over time, accounts get closed or consolidated with other accounts, property is sold, stocks get converted to cash, and retirement accounts get depleted. If a client fails to regularly update the inventory, there is a chance that an old inventory could create confusion and send you or the client’s loved ones down rabbit holes as you try to handle your client’s affairs. Assisting your client with this process can also help you discover accounts and assets that you could help them manage, consolidate, and simplify, thereby benefiting both you and your client.

Some people find it helpful to choose a specific date each year when they will review and update their inventory and also their estate planning documents. Whatever will work best for the client should be a part of the plan. The client should then implement the plan and stick with it.

Helping your client understand the great value that can be created through a simple but critical inventory will be a significant value-add that you can provide to the client and the client’s family. And when clients and their families benefit from such effort on their behalf, you can be confident that your business will continue to grow and prosper for years to come as multiple generations seek your professional advice. If you have any questions about how you can help your clients create and maintain an inventory, feel free to give us a call.